| Options for Liberalising Trade in Environmental Goods in the Doha Round |

|

| Tuesday, July 21, 2009 |

|

Paragraph 31(iii) of the 2001 World Trade Organization (WTO) Doha Ministerial Declaration calls for “the reduction or, as appropriate, elimination of tariffs and non-tariff barriers

Options for Liberalising Trade in Environmental Goods in the Doha Round, Section 2 of the paper examines environmental and trade effects of reduced tariffs on established environmental technologies for developed and developing countries. In Section 3, the environmental and trade effects are analysed for reduced tariffs on environmentally preferable products, including those based on process and production methods (PPMs). Section 4 outlines the current proposals on environmental goods in the Special Session of the CTE. Options for how to proceed are developed in Section 5. These include proposals to select crucial environmental imperatives, develop an environmental performance criteriabased approach, negotiate an environmental goods agreement in the WTO and put in place an environmental duty drawback system. Finally, Section 6 offers some conclusions and recommendations as a contribution to advance the debate. |

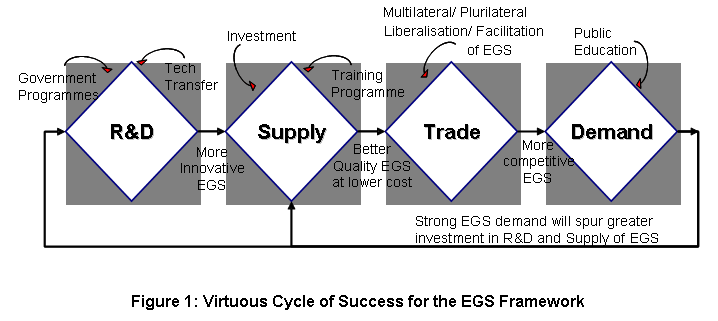

Submitted by Singapore

AIM

This paper seeks CTI's endorsement on a work programme framework for environmental goods and services (EGS) in APEC.

...

Submitted by Singapore

AIM

This paper seeks CTI's endorsement on a work programme framework for environmental goods and services (EGS) in APEC.

...