Normal 0 false false false MicrosoftInternetExplorer4

st1\:*{behavior:url(#ieooui) } /* Style Definitions */ table.MsoNormalTable {mso-style-name:"Table Normal"; mso-tstyle-rowband-size:0; mso-tstyle-colband-size:0; mso-style-noshow:yes; mso-style-parent:""; mso-padding-alt:0in 5.4pt 0in 5.4pt; mso-para-margin:0in; mso-para-margin-bottom:.0001pt; mso-pagination:widow-orphan; font-size:10.0pt; font-family:"Times New Roman"; mso-ansi-language:#0400; mso-fareast-language:#0400; mso-bidi-language:#0400;}

1 Abstract

It was presumed that the passage of NAFTA would stimulate considerable growth in markets for environmental goods and services in Mexico, and the rapid development of an environmental industry in Mexico. While the commercial activity of companies solving environmental problems is no sure measure of environmental quality, it is a valuable indicator of how both the private and public sector is responding to environmental challenges, as well as the impact that various policy instruments are having on environmental expenditures. This paper quantifies the growth and evolution of environmental market in Mexico since 1995, and characterizes the contribution of imports and Mexico’s own environmental industry.

While annual growth in the environmental market has been 5-10% since 1995, environmental companies say NAFTA played only a minimal role in driving growth. Environmental companies believe market demand could be much higher with better enforcement and indeed Mexico’s market evolution lags other nations. The Mexican environmental market has seen notable increases in activity since 1995, but imports have outpaced the development of Mexico’s environmental industry.

In the broadest terms, NAFTA has not brought proportionally more pollution to Mexico as many feared, but it is gradually bringing higher standards of environmental performance due to the influx of multinational firms operating under their own guidelines. The challenge is to turn these standards into the norm rather than the exception, and working with Mexican authorities to apply similar standards to their environmental infrastructure.

2 Executive Summary

To what extent has NAFTA been the driver of developments in environmental industry in Mexico since 1995? That is the fundamental question that guides the purpose of this paper. To be succinct, the answer is that NAFTA has played a role in driving the environmental market in Mexico, but only a minimal and mostly an indirect role.

NAFTA has spurred economic growth, the entry of multinational corporations into Mexico and some increased awareness and attention to environmental issues, and through this the environmental market has grown to an extent. On the other side, NAFTA has at least not resulted in Mexico being a ‘pollution haven’ as many feared as most foreign company entries into Mexico since 1995 have ‘imported’ their own corporate environmental standards and operating practices with them. The presence of more multinational firms have even had the effect of accelerating raising the baseline of voluntary environmental operating standards in Mexico in the opinion of several environmental companies interviewed for this paper, although this has yet to have a significant impact in driving market demand for environmental service and equipment companies.

Environmental regulations and their enforcement are the principle drivers of environmental business in the earlier stages of environmental market evolution in a still-developing nation like Mexico. Participants in Mexico’s environmental markets cite federal regulations and enforcement as by far the most influential market driver today, but also complain about a relative lack of enforcement in many segments of the market. Growth in the environmental market in Mexico has been between 5% and 10% annually since 1995, and although this growth has been faster than that of the Mexican economy overall, it still lags environmental market growth in other nations at a similar stage of development.

While in the environmental market in Mexico has grown at a respectable rate, the growth of the national environmental industry in Mexico has not grown at an equal rate, widening a trade deficit in environmental goods and services. The most recent research by EBI estimates a $5.1 billion environmental market in Mexico with a domestic environmental industry of $2.3 billion that accounts for few exports, and hence a $2.8 billion trade deficit. Filling the trade gap is largely the USA (US sales account for 27% of the Mexican market), although the rest of the world combined accounts for a slightly larger portion of Mexico’s environmental market at 28%.

Environmental companies operating in Mexico report increased cooperation amongst environmental industry companies from all countries, but also a higher level of competition as the market matures. More importantly, while Mexican companies have lost market share in the 10 years since NAFTA, their capacity to address a number of environmental problems has increased dramatically. The remaining challenges for the Mexican environmental industry to build capacity are to augment their evolving technical abilities with business acumen and furthering their relationships with the policymakers and direct customers they have in government to make a larger foundation for their business.

A questioner at the CEC Symposium in April 2008 where this paper was presented posed why has the growth of Mexico’s environmental industry not been as high as one may have expected and the answer has many elements: 1) as expected, relative free trade has left few barriers for environmental service and equipment providers to do business in Mexico; 2) a relative lack of qualified and experienced companies and people in environmental services in Mexico has hampered domestic growth; 3) sporadic investments by municipal and federal governments on programs for water, wastewater, air quality and waste and last and perhaps foremost 4) a strong domestic environmental industry depends on consistent demand provided by consistent and predictable environmental regulations and enforcement by the local government.

Separately from environmental companies, government agencies themselves must make environmental conditions a higher priority and begin to take some notice that the environmental industry participants that serve them can also serve as a distinct constituency for them. In other words the environmental industry community has both the environmental quality interests of the government and citizens and the economic and business interests of the private sector in balance to assure continuity in their business. A step further for government is the realization themselves that a capable and growing national environmental sector is largely dependent on predictable and consistent environmental policy, regulation and enforcement from the government, and that spending by the regulated community often leads to revenues for a growing domestic service industry.

In conclusion, the decade since NAFTA was passed has seen changes in Mexico’s environmental market and its environmental industry. But while these changes may not have been dramatic, nor principally the result of NAFTA, they are part of a fairly predictable pattern of evolution of environmental markets and industries. NAFTA has served to accelerate some components like the entry of multinationals and the increased transparency required of them operating in a still emerging economy, but it has not had the impact of institutionalizing environmental quality across federal, state and local government and the nation—not that NAFTA was intended to do this, of course. Consistent environmental markets emerge over more than a course of 10 years and while NAFTA has accelerated the process, there is still a ways to go.

2.1 Data Highlights

- The environmental market in Mexico grew 8% in 2006 to reach $5.1 billion.

- The environmental market in Mexico grew 84% from 1995-2005 from $2.6 billion in 1995 to $4.7 billion in 2005.

- The environmental market in Mexico accounted for 0.59% of Mexico’s gross domestic product (GDP) in 2006, up from 0.44% in 1995

- The environmental industry in Mexico accounts for about 44% of the Mexican market (or 56% is imports, mostly from the USA), representing $2.3 billion in revenues. Mexican environmental exports were only $80 million in 2006, but have grown from $50 million in 2001.

- In just services, the environmental industry in Mexico accounts for about 50% of the Mexican market, representing $1.2 billion in revenues in 2006.

- Foreign direct investment in Mexico remained fairly consistent from 1995-2005 (64% from the USA for the 10-year period), with the exception of a spike in 2001 resulting mostly in the financial services industry. While official statistics on FDI make no mention of environmental services, interviews with companies indicate very modest investment and some movement of persons, but mostly the transfer of expertise and the hiring of local personnel.

- EBI Survey Results: In general environmental companies say NAFTA has played only a minimal role in driving growth of the Mexican environmental market. Survey respondents rated NAFTA only 8th out of 12 market drivers, well behind regulations, enforcement, global standards of multinationals, overall economic growth and even media coverage.

- EBI Survey Results: Environmental companies rated foreign-owned companies as customers as contributing to environmental market growth significantly more than Mexican companies with 60% rating growth from foreign-owned companies as ‘high’ or ‘very high’, and 90% rating growth from Mexican companies as ‘modest’ or ‘little growth’. By customer type the top five in the rankings for pacing growth from 1995-2005 were: oil & gas, light industry/automobiles, heavy industry (chemical, steel, paper, etc.), tourism, construction & development; at the bottom were agriculture, local/city government and state government.

- EBI Survey Results: In general, environmental companies rated the activity level of Mexican, US and Canadian firms in Mexico as increasing noticeably from 1995-2005. While 63% of respondents characterized the market in 1995 as having ‘no competition’ or ‘very little competition’, only 7% characterized it as having ‘no competition’ or ‘very little competition’ in 2005.

- EBI Survey Results: Environmental companies have seen noticeable increase in the technical capacity of the domestic environmental industry in Mexico from 1995-2005. A majority (61%) of respondents characterized the Mexican environmental industry as having a “low level of capacity to address only a few types of environmental problems” in 1995. In 2005 a plurality (48%) of the same respondents characterized the Mexican environmental industry as having a “moderate level of capacity to address many types of environmental problems” and 19% said a “high level of capacity to address a few types of environmental problems.”

Submitted by Singapore

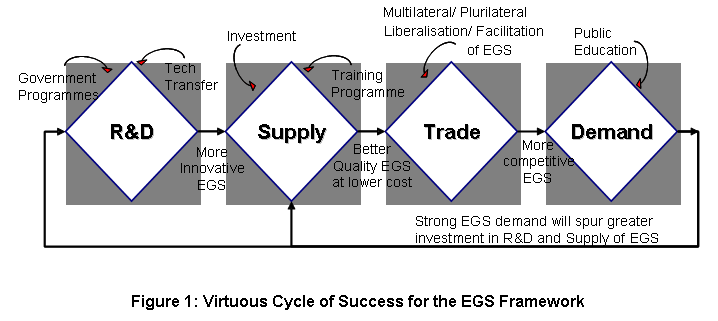

AIM

This paper seeks CTI's endorsement on a work programme framework for environmental goods and services (EGS) in APEC.

...

Submitted by Singapore

AIM

This paper seeks CTI's endorsement on a work programme framework for environmental goods and services (EGS) in APEC.

...