| WTO Negotiating Strategy on Environmental Goods and Services for Asian Developing Countries |

|

| Tuesday, July 21, 2009 |

|

The key to successful negotiations lies in the ability and capacity of the negotiating participants to feel that it can result in a “win-win” mutually beneficial outcome for all concerned – or in the case of the WTO environmental goods and services negotiations, a “win-win-win” outcome for trade, environment, and development. This means that participants must be willing to adopt “integrative” approaches to the negotiations – i.e. the participants must be willing to work towards a negotiated outcome that addresses their respective interests in an integrated manner.

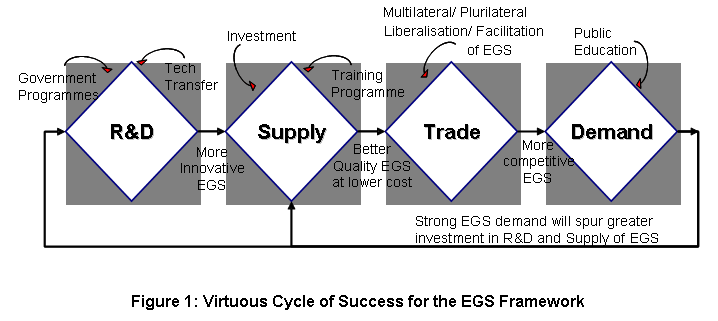

WTO Negotiating Strategy on Environmental Goods and Services for Asian Developing Countries, In 2005, the global environment industry was estimated to be USD607 billion, with the US, Western Europe and Japan together accounting for 84 percent of this market. The global exports of environmental goods (EGs), as classified by the OECD list, for 2002 was estimated to be USD238 billion. An UNCTAD study has pointed out, that “developing countries have an important export surplus with developed countries in a number of groups of EGs, in particular EPPs, including manufactured apparel from natural cotton fibers, apparel manufactured from natural wool and silk fibres, wood and wood-based products, clean fuels and renewable energy, other Type A EGs [these include manufactured goods and chemicals used directly in the provision of environmental services], and the core list of EPPs.” In terms of sectors of the global environmental market, the environmental services (ES) sector (including resource management and energy) is much larger than the goods sector. In 2001, environmental services accounted for 78 percent of the total market by value. |

Submitted by Singapore

AIM

This paper seeks CTI's endorsement on a work programme framework for environmental goods and services (EGS) in APEC.

...

Submitted by Singapore

AIM

This paper seeks CTI's endorsement on a work programme framework for environmental goods and services (EGS) in APEC.

...